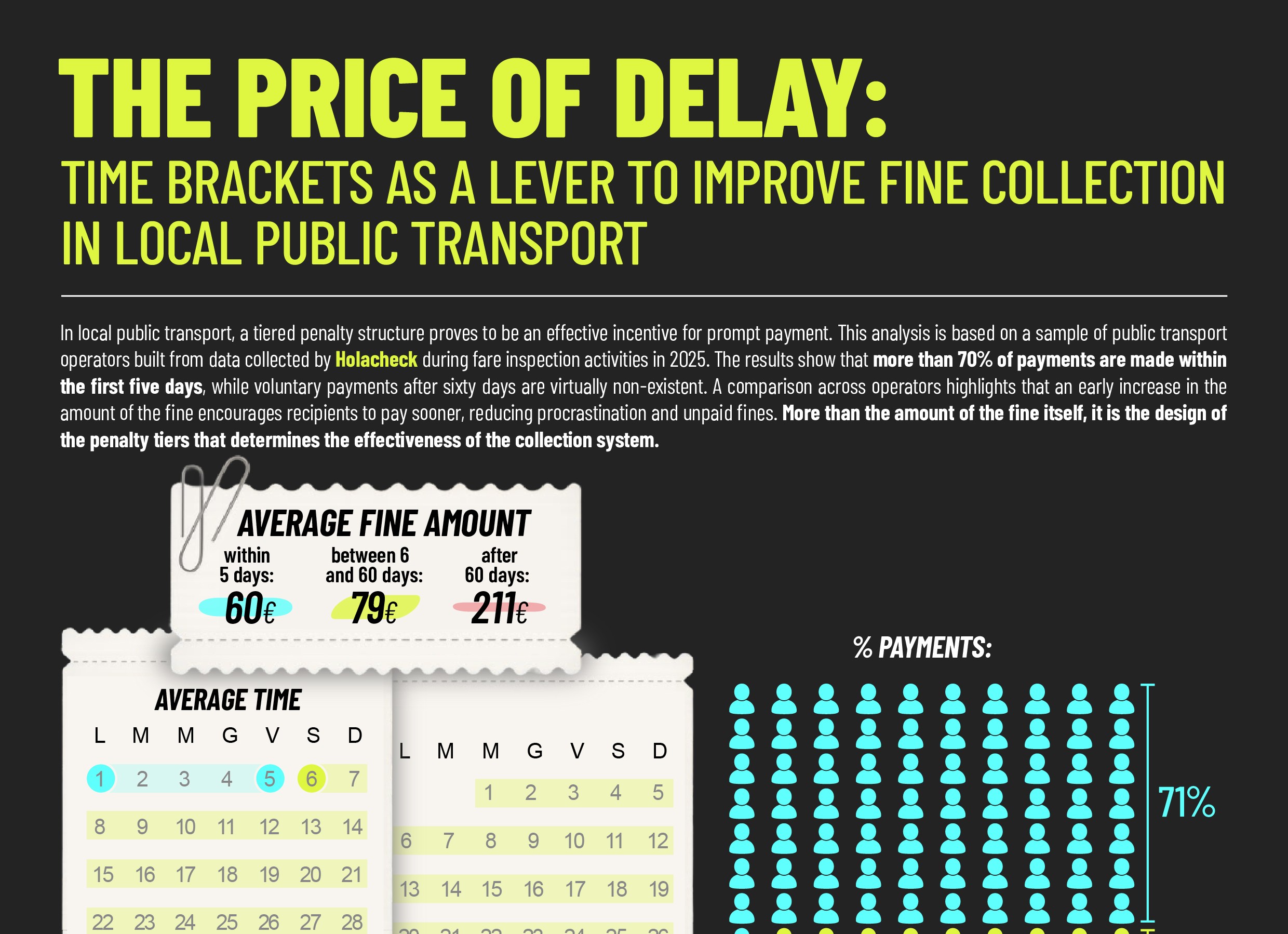

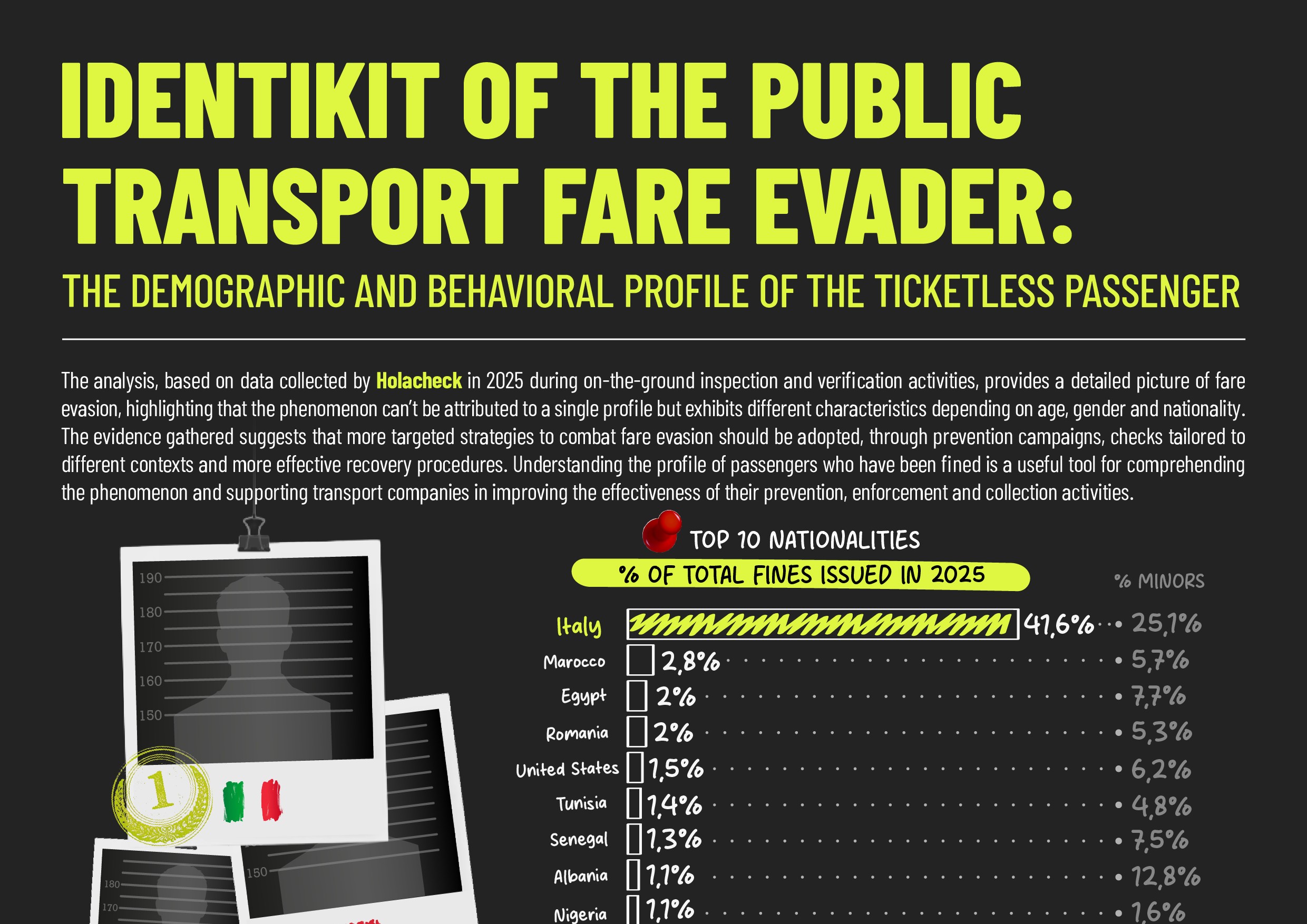

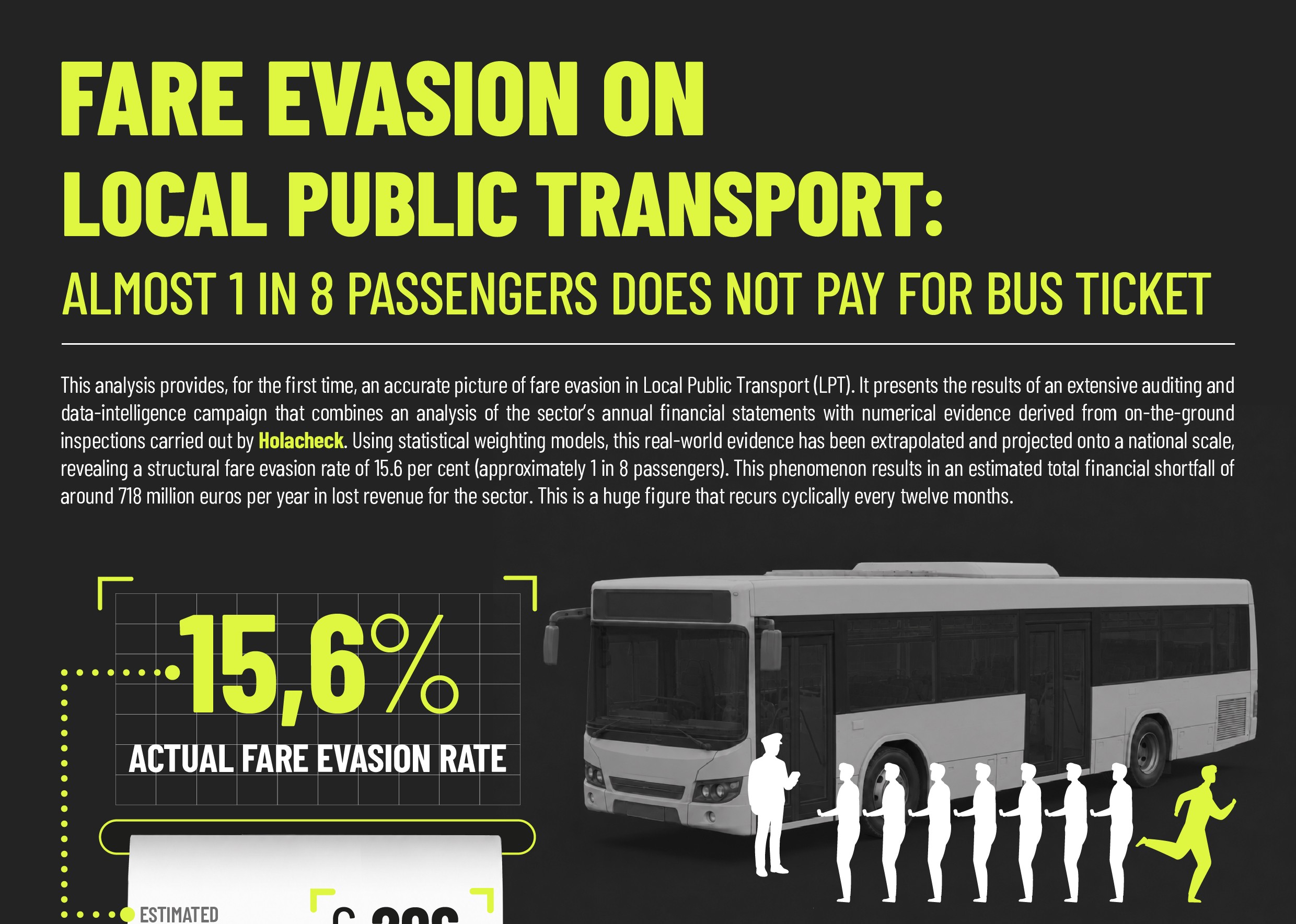

Italy, although the leading bus market in Europe and among the leaders in terms of new registrations in 2024, has progressively lost production capacity, with most vehicles now made abroad, with rare exceptions. This situation highlights the lack of an industrial policy that focuses on enhancing national production capacity.

Share on:

According to ANFIA data, bus registrations in Italy in 2024 totalled 6,594, up 26.7% over the previous year. However, historic brands such as Iveco have progressively focused their production capacity abroad, with plants located in France and the Czech Republic. Menarinibus maintains production entirely in Italy, with plants operating in Bologna and Flumeri.

Bus fleet in Europe: Italy first for circulating vehicles

According to the ACEA report - Vehicles on European Roads published in January 2025, the number of buses on the road in Europe fell from 679,286 in 2019 to 662,142 in 2020 (-2.5%), and then gradually rose again: 667,164 in 2021, 673,307 in 2022 and 679,801 in 2023. The overall growth over the five-year period is +1.0%.

In 2023 Italy is the country with the highest number of buses in circulation: 100,078 units, equal to 14.7% of the European total. It is followed by France (93,928, 13.8%), Germany (84,628, 12.4%), Poland (81,754, 12.0%) and Spain (62,881, 9.2%).

The countries with the lowest values include Luxembourg (2,649), Slovenia (2,197), Cyprus (3,099) and Estonia (3,666), each with between 0.3% and 0.5%.

A comparison with 2019 shows significant increases in Luxembourg (+19.3%), Portugal (+12.5%) and Romania (+6.2%), while the most marked negative changes are in Ireland (-36.8%), Estonia (-29.8%) and Finland (-11.9%).

Evolution of the bus fleet in Europe (2019-2023)

Note: Data from Bulgaria and Malta not available

Registration 2024: upward trend, Italy ranks second in Europe

Nel 2024 sono stati immatricolati 45.867 autobus in Europaby registering a growth of +14,8% rispetto al 2023 (39.953 unità). I cinque principali mercati per volumi sono:

- United Kingdom 8.657 units (18.9%)

- Italy6.594 units (14.4%)

- France6.258 units (13.6%)

- Germany5.382 units (11.7%)

- Spain4.059 units (8.8%)

Together, these five countries account for 67.4% of European registrations in 2024. Among the strongest growth figures are the UK (+56.7%), Italy (+26.7%), Poland (+26.4%) and Spain (+10.3%).

In total, the ten largest markets accounted for 36,326 registrations (79.2% of the European total).

Note: Data refer to EU, UK and EFTA (European Free Trade Association) countries

Italian market and domestic production: between concentration and new dynamics

In the Italian market, the top ten manufacturers account for 88.4% of total registrations in 2024, or 5.831 units, while in 2023 their share was 88.3%, with 4.597 vehicles.

In detail, the brand with the highest number of registrations in 2024 is Iveco, with 2.930 units, or 44.4% of the total. It is followed by Mercedes Benz with 878 units (13.3%), Solaris with 551 units (8.4%), Otokar with 314 units (4.8%) and Menarinibus with 285 units (4.3%).

The next positions are occupied by Ford (262 units, 4.0%), MAN (184 units, 2.8%), Scania (181 units, 2.7%), Karsan (134 units, 2.0%) and Setra (112 units, 1.7%). The ‘Other’ category, which brings together manufacturers not included in the top 10, totalled 763 registrations in 2024, or 11.6% of the total, compared to 608 units in 2023 (11.7%).

First place therefore goes to Iveco, historically one of the main Italian manufacturers, which has progressively located its production capacity abroad, with plants in Annonay (France) and Vysoké Mýto (Czech Republic). However, in 2023, a new pole was activated in Foggia, with a line dedicated to the assembly of buses, also supported by investments under the National Recovery and Resilience Plan (PNRR).

Menarini (former Industria Italiana Autobus), part of the Seri Industrial group, is among the top ten manufacturers with 285 registrations in 2024. The company maintains production entirely in Italy, with plants operating in Bologna and Flumeri. The company, engaged in the development of electric buses in synergy with FIB S.p.A., is currently at the centre of negotiations for the sale of 25% to the Chinese group Geely .

Alongside the big brands, other Italian companies have maintained an independent industrial presence, as in the case of Rampini Carlo S.p.A., with headquarters and production in Passignano sul Trasimeno. The company specialises in the production of small and medium-sized electric and hydrogen buses. In 2024 it registered 48 buses, a number that does not allow entry into the national top 10, but which is accompanied by an established presence in foreign markets.

The Italian bus market therefore represents a significant share at European level, both in terms of circulating fleet and annual registrations. National production, although showing signs of recovery, is today limited and highly concentrated.

For more insights, also read the focus on profitability margins in the LPT sector.